A brief history of MIS systems in education... and the future possibilities

MIS (which stands for Management Information System) – is a key tool in schools, that handles the majority of data within schools, a kind of CRM for education – assessment, attendance, timetable, communication, behaviour, payments, safeguarding, exams, SEND, communications and HR data are often stored within it to name a few functions.

For decades, this area of the market was dominated by SIMS. The only development in managing data were products that integrated with SIMS, a whole market within itself – software that did elements that SIMS did, but better.

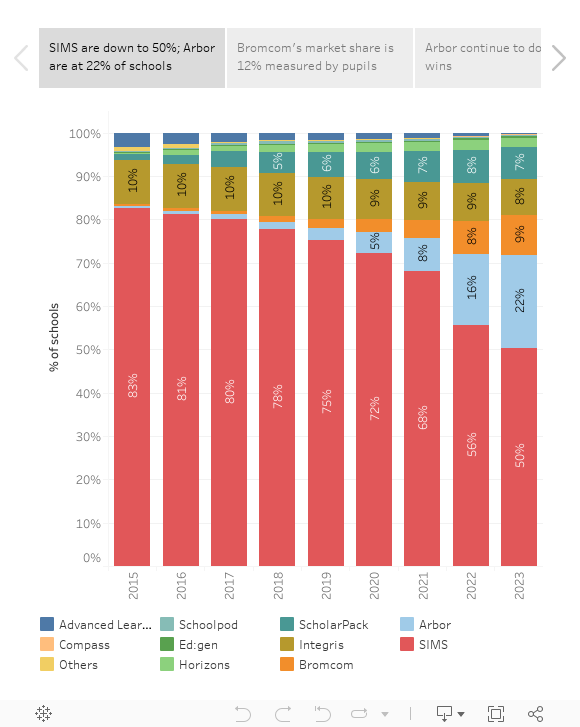

From 2010, through to 2017, for example, SIMS Market share never dipped below 80% in the UK. However, in 2023 it sits at just 50% according to data from the excellent Bring More Data.

The current picture

This reduction of market share appears to be due to SIMS failure to migrate their systems to a cloud platform in an effective way and the emergence of cloud-based alternatives. The Key, owners of Arbor, ScholarPack, and Integris alongside Bromcom, Iris Ed:gen, and Compass all have seen their market share continually rise.

SIMS, with over 80% of the market share for over 10 years, formerly part of Capita, was sold to EES and became part of the ParentPay family in 2021- and had been promising SIMS Primary since January 2018 – their initial cloud offering, which never materialised into a real product.

Following the takeover, SIMS Next Gen was promised as a result of a £40 million investment in moving to the cloud, this would be achieved by moving SIMS to the cloud in modules (or slices as they are called).

And, whilst progress has been achieved with Next Gen in some areas, this delay has led to a huge decline in market share. The product is still predominantly on-premise with cloud elements.

Further decline in market share has been seen from an attempt to lock in customers to 3-year deals and prevent migrations.

It’s been refreshing, therefore, to see comprehensive competition in the MIS market in the UK, following decades of stagnation. Where the only ever real competition was between systems which patched into SIMS data.

There are 2 main players in the market these days of cloud MIS, Arbor, and Bromcom, Arbor is a relative newcomer to the market, and Bromcom with decades of prior experience.

The Key owns Arbor which now has 22% of the market – but they also own Integris (8%) and one of the first entrants into the post SIMS era – ScholarPack (7%) – which gives them a 37% market share overall.

Arbor, once a primary favourite now appeals across the board, including their recent developments in the MAT sphere, bringing trusts data together at a high level for visibility. Their system is a lot different from SIMS, with a different way of achieving tasks, using contextually aware information and a suite of powerful tools.

It will be interesting to see if ScholarPack and Integris are merged into a single Arbor product, as it certainly has the clout to absorb – showcased by their growth into Arbor over the last few years – but it can’t be a feature loss scenario, so I’d imagine Arbor will make sure their system can support the users of their other platforms effectively before forcing a migration, but some customers are already making the move.

Bromcom have the largest (non SIMS) share of secondary schools, and is a name with quite a bit of history in edtech – pioneering electronic registers – and interestingly their platform has a 12.5% of the market share when measured by students, but despite considerable growth in 2023 of 368 schools, they still lag behind Arbor quite considerably.

However, their product has had considerable success with trusts and continues to grow rapidly.

Other providers are making significant developments, the notable of the rest is Iris who have launched Ed:Gen to complement their more established iSAMS platform, and last year hit over 100 schools.

From feedback from users, Arbor seems to be the way to go if you want a complete refresh of your MIS experience – and it has been very successful in primary for that reason, however, Bromcom has roundly been considered to be more feature-complete at secondary level – and is preferred by exam officers and timetablers.

In reality, I have seen primary and secondary schools (and a mix of both in many trusts) adopt either platform successfully.

Poor migration and adoption experiences generally stem from existing poor data within incumbent systems, or a lack of appetite to change within key staff areas (such as exam managers, and data managers). Additionally, failure to plan and allow for training within the schools is another leading cause of poor experience.

It’s interesting to see how both Arbor and Bromcom are actively engaging to improve these areas in unique ways.

Why the change?

The key driver for the success of Bromcom and Arbor is cloud computing, allowing considerable real-time cost and time savings for schools and removing the need for dedicated hardware and infrastructure to locally host a platform and its maintenance and complex management.

Cloud computing allows the providers to manage the system, and add features much easier than locally hosted systems, reducing support costs of having to support hundreds of custom setups.

However, many schools are yet to get, or take wider advantage of the cloud elsewhere in their setups, meaning both systems struggle to integrate with older, non-cloud tech – the APIs are there, however – and newer versions of software do interact, the problem as we all know – is schools don’t get the latest versions for many years after release in many cases!

The good news here is that the tide is turning, and cloud adoption continues to be successful for schools, with increased accessibility and availability to improving education-focused improvements. With the generally good experiences schools are having with Cloud MIS platforms, they can be a real driver of wider change. Which works for everyone.

The systems also have a growing feature set, which means schools don’t need multiple systems. This can be a good thing – cheaper, and interlinking data between key components and for reporting – but also means that we are still waiting for many of these areas to reach the maturity of existing market leaders (think safeguarding options in the MIS, compared to CPOMS and My Concern, for example).

Finance integration is a key driver here, with both Arbor and Bromcom focusing on this area (Bromcom natively, Arbor through the purchase of RM Integris) – now the finance market for schools is a lot more open. Some systems are fully cloud, but many are not. Including SIM’s own FMS which still is out there, and I don’t quite know how after even SIMS tried to replace it.

Arbor did well to become the leading MIS without finance, but Bromcom feedback I have heard is that schools have gone to it for a complete solution.

What does this all mean?

Being such a core part of any school or trusts day to day operations, as well as providing all the data for strategic overview and planning, the changes in the MIS market are important to note, but this is just the start of a period of wider change which has emerged I think, as schools and trusts realise they are no longer wedded to a platform for life.

It’s within all the new players’ best interest to ensure that schools can move into their platforms, and out of their competitors easily – something that was never really possible before – and something that SIMS is still trying to actively stop.

However, my belief is the churn between the platforms will start to increase, and specific features (not least the adoption of AI to understand these large data blocks) and built-in features such as finance – will probably make it a lot easier for each provider to attract and switch customers into their platform.

It also means we are likely to see, as SIMS market share continues to decline (as it is still the largest provider), new entrants into the market in the next 10 years, that we did not see before.

Although saying all this, with the Key buying up several tools, we have seen a stabilisation for now – whilst product features are enhanced, and expanded. For example, the main reason Arbor purchased RM Integris, was RM Finance which is being rolled out as Arbor Finance to compete with Bromcom’s finance package. It’s likely, with their current growth, that Arbor will surpass SIMS market share by the time they fully move to SIMS Next Gen – but the longevity of customers staying will be determined by three factors – reliability, features, and support.

Schools hold an incredible amount of data, and one of the exciting areas of development has been that data becomes accessible and usable live in the application, and in-depth and customisable reporting using the data. This is an area that we will continue to see huge impacts within education – bringing this data to the fore, and allowing schools to make data-driven decisions in a real-time sense, something that has not been possible before their introduction on a wide scale without experienced data managers.

It’s certainly a very interesting time to see the changes we have seen over the last few years, and where now we go, it’s unchartered territory.

If you want to hear more about Arbor, I had a great chat with Beth from Arbor on my podcast!